Will the Debt-Ceiling Drama Affect Money Markets?

Tax-Proof Your Estate

Adviser Market Update

Company News

Strategy Activity Update

Will the Debt-Ceiling Drama Affect Money Markets?

The news has been unavoidable: The U.S. is drawing closer to a possible collision with the debt ceiling. We believe a default is highly unlikely, but we also understand why you might find the situation unsettling. In fact, over the last few weeks, we’ve received some questions from clients about the potential ramifications for money market funds should Congress fail to act on the debt limit—and that was before bond ratings service Fitch issued its warning that the U.S. is at risk of a credit downgrade due to the ongoing horse-trading in Washington.

The bottom line is that money market funds are considered some of the safest places to hold cash reserves. Yet they invest in short-term and ultra-short-term bonds, with many set to mature starting in June—when the U.S. would hit the debt ceiling absent congressional action.

So, are they still safe? Our research team spoke to managers at some of the largest money market funds owned by our clients. Here are the takeaways:

First, the managers we spoke with do not own any Treasury securities that will mature during the possible debt-ceiling deadline window (June through August). So in these portfolios, there are no Treasury holdings that would be impacted by a default or delayed payment.

Next, these managers are taking advantage of the Federal Reserve’s “overnight lending facility.” This facility is essentially a one-day loan to the Fed that matures daily and is backed by U.S. Treasury bonds from the Fed’s balance sheet. Any loan to the Fed represents liquidity that is available to the money market the next day.

The managers said they have anywhere between 40% and 55% of fund assets (representing billions of dollars) in these daily loans to the Fed’s overnight facility. In other words, a significant chunk of fund assets is available for redemption daily. In the event of a default, funds that are using this facility will have ample liquidity to meet large shareholder withdrawals, should they occur.

Finally, like us, these managers feel confident that despite the messy negotiations, the two sides will ultimately work out a deal so that the U.S. can make good on its financial obligations to creditors.

To learn more about bonds and their risks, we encourage you to check out our Bond Basics special report, which should help put some of the stories about default and debt issuance in context for you.

Tax-Proof Your Estate

Estate planning parlance is chock-full of acronyms. We recently wrote about SLATs and CRTs, and there’s another we’d like to share: DSUE, or deceased spousal unused exclusion.

According to our manager of financial planning, Andrew Busa, the DSUE is one of the most important financial planning tools, but most people have never heard of it. Why is the DSUE so notable? It maximizes estate benefits for high-net-worth married couples.

The current federal gift and estate tax exemption for individuals is $12.9 million—and it’s twice that for married couples. With a DSUE, the estate of a surviving spouse can benefit from the unused portion of the decedent’s exemption, thereby shielding additional assets from estate tax. Also known as a “portability election,” this combined exemption maximizes benefits for families that would otherwise contend with a top estate tax rate of 40%.

And keep in mind that the federal gift and estate tax exemption for individuals is scheduled to revert to $5 million (subject to inflation indexing) in 2026—meaning many more families may benefit from portability.

If there is a reasonable chance that your estate may exceed the federal estate tax exemption, your advisor can discuss the logistics of filing the tax paperwork to make a portability election in the future. It’s an admittedly complicated and often costly process, but it could also be one of the more consequential financial planning moves you can make if your estate qualifies.

Adviser Market Update

Here are some of the things our research team is watching this week and why they matter:

Economic activity increased in May at the fastest pace in 13 months. The service sector continues to enjoy strength in the aftermath of the worst of the pandemic, though manufacturing has slumped as consumers shift their spending from goods to services. However, the leading economic index (a gauge of 10 indicators compiled by the Conference Board) did not paint as rosy a picture in April. It posted a 0.6% monthly drop, indicative of a potential recession looming later this year or early next year.

The housing market continues to be hampered by the Fed’s interest-rate hikes. Mortgage rates rose to their highest level in two months this week and the index of homebuying applications fell to its lowest point since early March. In April, the slackening demand saw home prices post their biggest annual drop in more than 11 years. These are all important considerations if buying or selling a home is part of your near-term financial plan.

So far markets haven’t panicked as the debt-ceiling deadline (mentioned above) draws closer, but every day brings a heightened risk of volatility. The S&P 500 hit its 2023 high last week, though it’s given up some gains as debt negotiations continue. We know it can be upsetting to see this play out, and we’re prepared to take action should a default become more likely.

Company News: Adviser Joins Forces With Ropes Wealth Advisors!

In case you missed the exciting news last week: We have agreed to acquire Ropes Wealth Advisors, a distinguished Boston-based firm that provides estate and financial planning services to families, trusts and institutions. Adviser and Ropes Wealth are highly complementary companies when it comes to vision, values and longtime commitment to delivering exceptional service. This excellent cultural and strategic match will enable us to enhance our wealth management offerings in the future. We look forward to all that we can achieve together once the partnership becomes final in August.

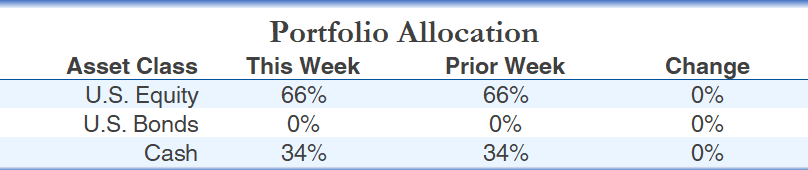

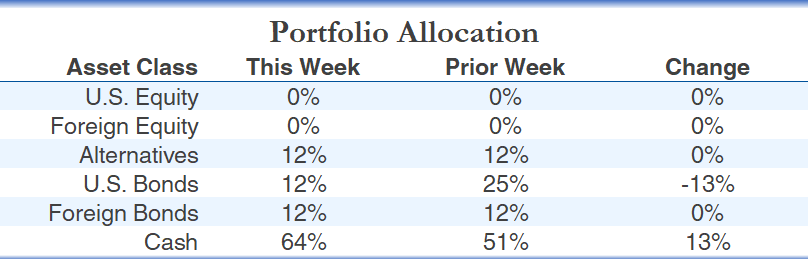

Strategy Activity Update

Please see below for a summary of the trades we executed over the week through Thursday and our current tactical strategy allocations.

Dividend Income

No trades

AIQ Tactical Global Growth

Sell Cash

Buy Fidelity MSCI Information Technology Index ETF (FTEC)

AIQ Tactical Defensive Growth

No trades

AIQ Tactical Multi-Asset Income

Sell iShares 7–10 Year Treasury Bond ETF (IEF)

Buy Cash

AIQ Tactical High Income

Sell iShares 0-5 Year High Yield Corporate Bond ETF (SHYG)

Sell iShares Broad USD High Yield Corporate Bond ETF (USHY)

Sell Xtrackers USD High Yield Corporate Bond ETF (HYLB)

Sell VanEck Fallen Angel High Yield Bond ETF (ANGL)

Buy Cash

If you’d like to learn more about our tactical or fundamental strategies, please contact Steve Johnson at 844-587-7393 or info@advisercapital.com.

Please note: This update was prepared on Thursday, May 25, 2023 prior to the market’s close.

This material is distributed for informational purposes only. The investment ideas and opinions contained herein should not be viewed as recommendations or personal investment advice or considered an offer to buy or sell specific securities. Data and statistics contained in this report are obtained from what we believe to be reliable sources; however, their accuracy, completeness or reliability cannot be guaranteed.

Purchases and sales of securities listed above represent all securities bought and sold in each strategy during the period stated. Each strategy’s portfolio generally includes more holdings in addition to the transactions listed above and in some cases the securities listed above may only represent a small portion of the particular strategy’s complete portfolio. Further, the securities listed above are not selected for listing based on their investment performance; thus it should not be assumed that any of the securities listed above were profitable or will be profitable, nor should it be assumed that future recommendations will be profitable. Clients and prospective clients should only make judgements about a strategy’s performance after reviewing the strategy’s composite performance information. There is no assurance that each security listed above will remain in the strategy’s portfolio by the time you have received or read this email. Securities are listed for informational purposes and are not intended as recommendations. Existing investor accounts may not participate in all transactions listed above due to each account’s particular circumstances.

Our statements and opinions are subject to change without notice and should be considered only as part of a diversified portfolio. You may request a free copy of the firm’s Form ADV Part 2, which describes, among other items, risk factors, strategies, affiliations, services offered and fees charged.

Past performance is not an indication of future returns. Tax, legal and insurance information contained herein is general in nature, is provided for informational purposes only, and should not be construed as legal or tax advice, or as advice on whether to buy or surrender any insurance products. Personalized tax advice and tax return preparation is available through a separate, written engagement agreement with Adviser Investments Tax Solutions. We do not provide legal advice, nor sell insurance products. Always consult a licensed attorney, tax professional, or licensed insurance professional regarding your specific legal or tax situation, or insurance needs.

Companies mentioned in this article are not necessarily held in client portfolios and our references to them should not be viewed as a recommendation to buy, sell or hold any of them.

Third-party publications referenced in this article (e.g., Citywire, Barron’s, InvestmentNews, CNBC, etc.) are independent of Adviser Investments. Readers should note that to the extent any third-party publication linked to in this piece also contains reference to any of the newsletters written by Dan Wiener or Jim Lowell, such references only pertain to the respective newsletter(s) and are not reflective of Adviser Investments’ investment recommendations or portfolio performance. Newsletters are operated independently of Adviser Investments. Opinions and statements contained in third-party articles are for informational purposes only; they are not investment recommendations.

The Adviser You Can Talk To Podcast is a registered trademark of Adviser Investments, LLC.

The Adviser Capital logo is a registered trademark of Adviser Investments, LLC.

© 2023 Adviser Capital, an Adviser Investments, LLC company. All Rights Reserved.